Germany

View:

May 15, 2024

Eurozone: Consumers - Still Missing?

May 15, 2024 10:34 AM UTC

Revised national account data confirmed the upside surprise in the preliminary data with EZ GDP rising 0.3% q/q. The question is whether this emergence from the modest H2 2023 recession is the start of more sustained momentum. We think not, mainly due to what are still weak consumer fundamentals

April 30, 2024

Eurozone Data Review: Less Weak But Soft Domestic Demand Taking Less Toll on Core Inflation?

April 30, 2024 9:29 AM UTC

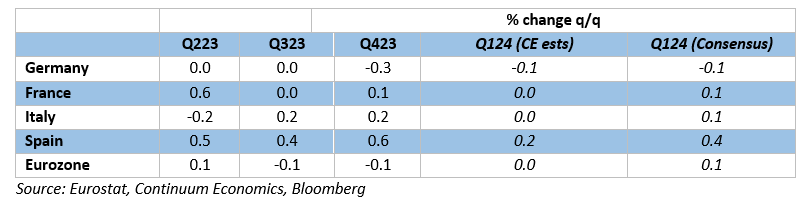

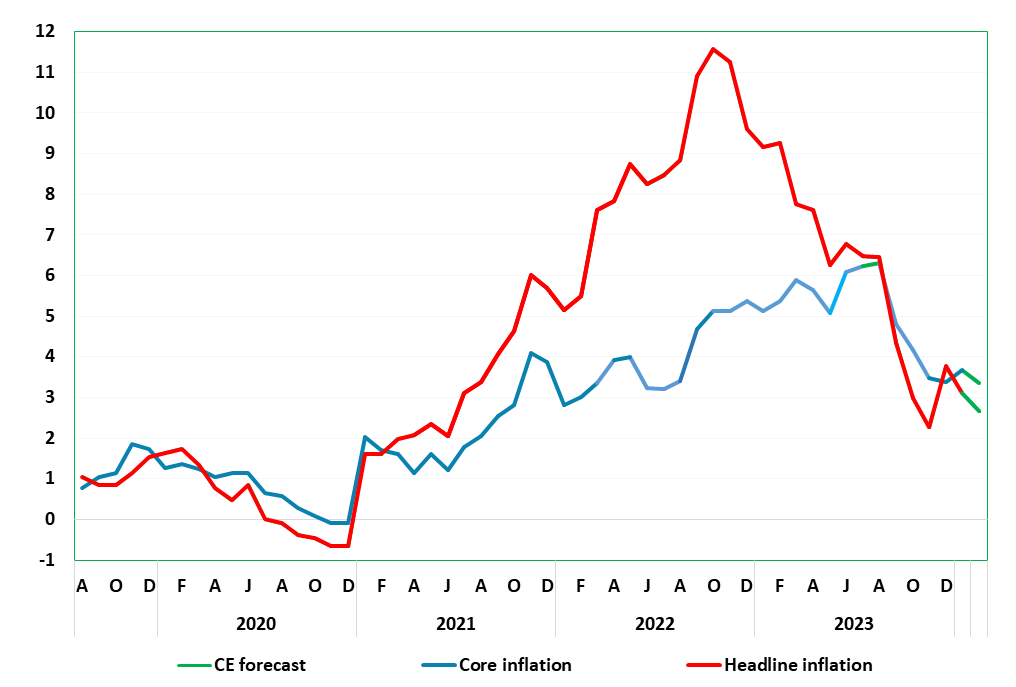

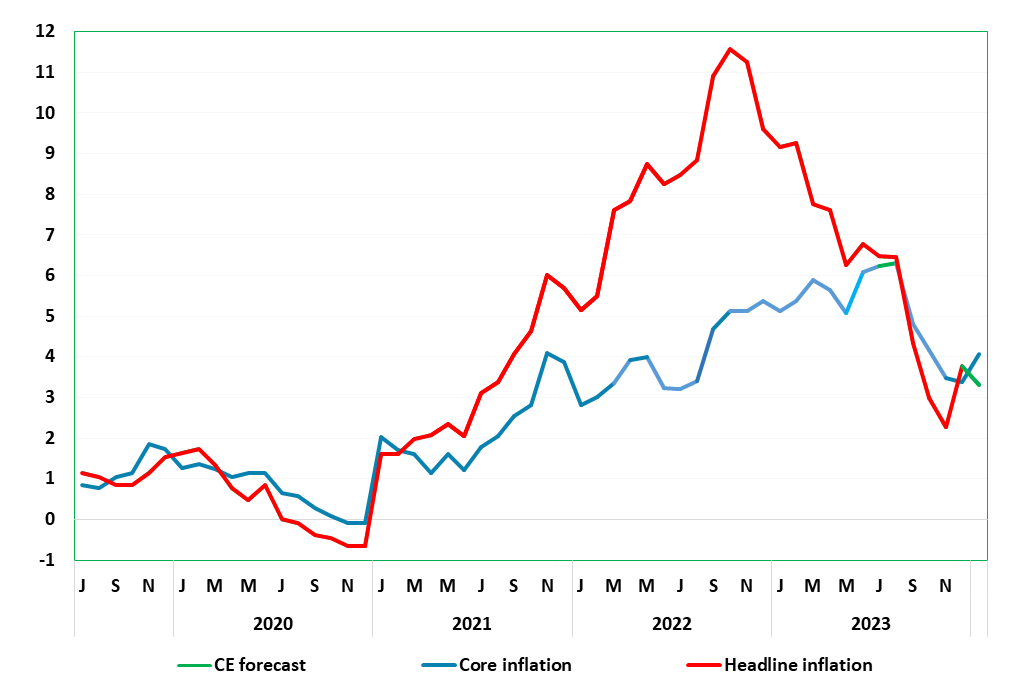

According to revised official national accounts data, the EZ economy was in recession in H2 last year, albeit modestly so and against a backdrop of marked, if not increasing, national growth divergences. This geographical variation continued into Q1 (Figure 1) where the flash GDP reading exceeded ex

April 29, 2024

German Data Review: Inflation Edges up Amid Less Resilient Services and Core Rate?

April 29, 2024 12:38 PM UTC

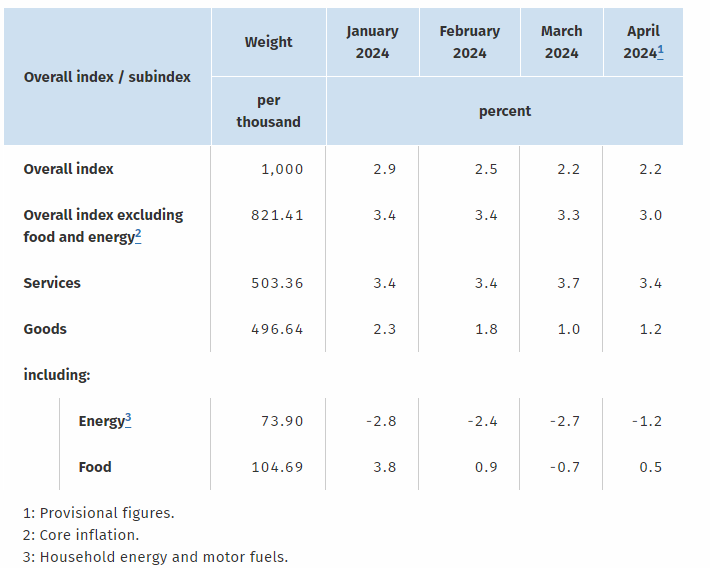

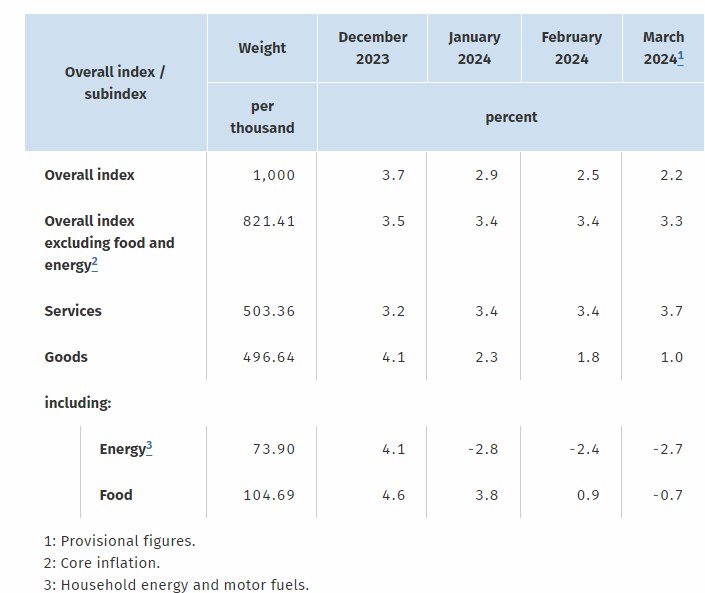

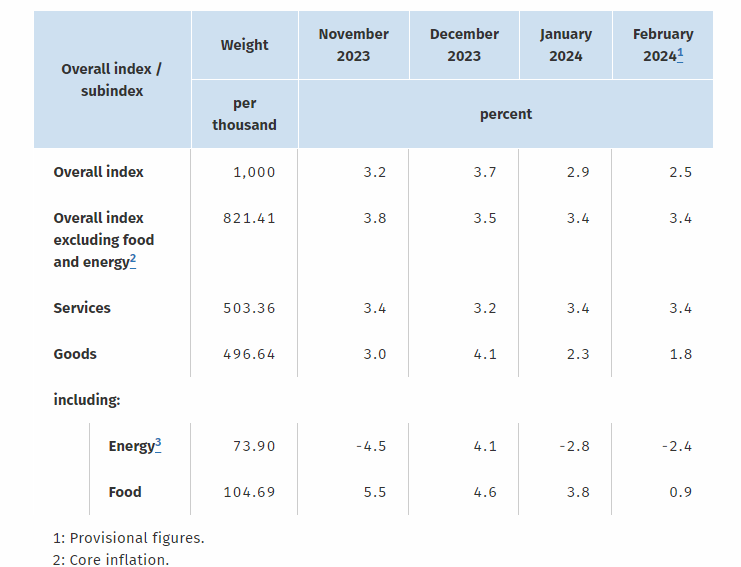

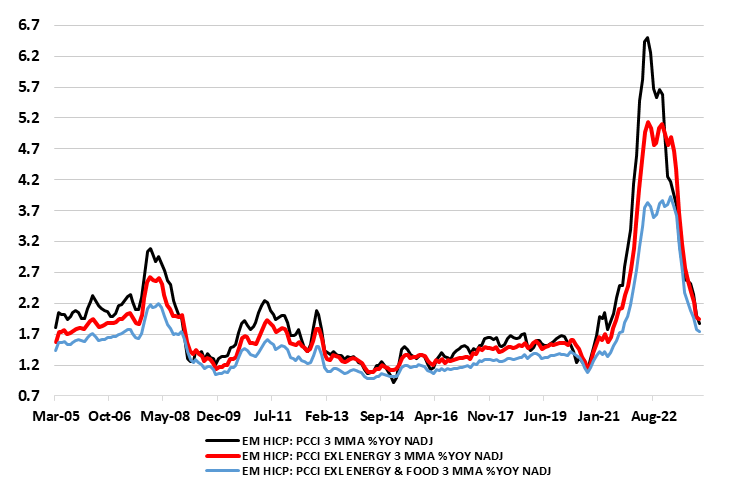

As we have repeatedly underlined, base effects continue to distort the German HICP/CPI readings, but the March data came in a notch below expectations for a third successive month. Indeed, it fell from 2.7% to a 33-month low of 2.3% in the March HICP data, dominated by a clear fall in food inflati

April 26, 2024

Headwinds To Long-term Global Growth

April 26, 2024 9:30 AM UTC

Bottom line: While much focus is on the cyclical economic position to determine 2024 monetary policy prospects, the 2025-28 structural growth trajectory differs to the pre 2020 GDP trajectory for major economies. While global fragmentation has a role to play, aging populations are already having a

April 24, 2024

Eurozone GDP Preview (Apr 30): Less Weak?

April 24, 2024 11:06 AM UTC

According to revised official national accounts data, the EZ economy was in recession in H2 last year, albeit modestly so and against a backdrop of marked, if not increasing, national growth divergences. This geographical variation is likely to have continued into Q1 (Figure 1) where we see a flat o

April 23, 2024

EZ HICP Preview (Apr 30): Core Disinflation Signs to Flatten Out Further?

April 23, 2024 9:43 AM UTC

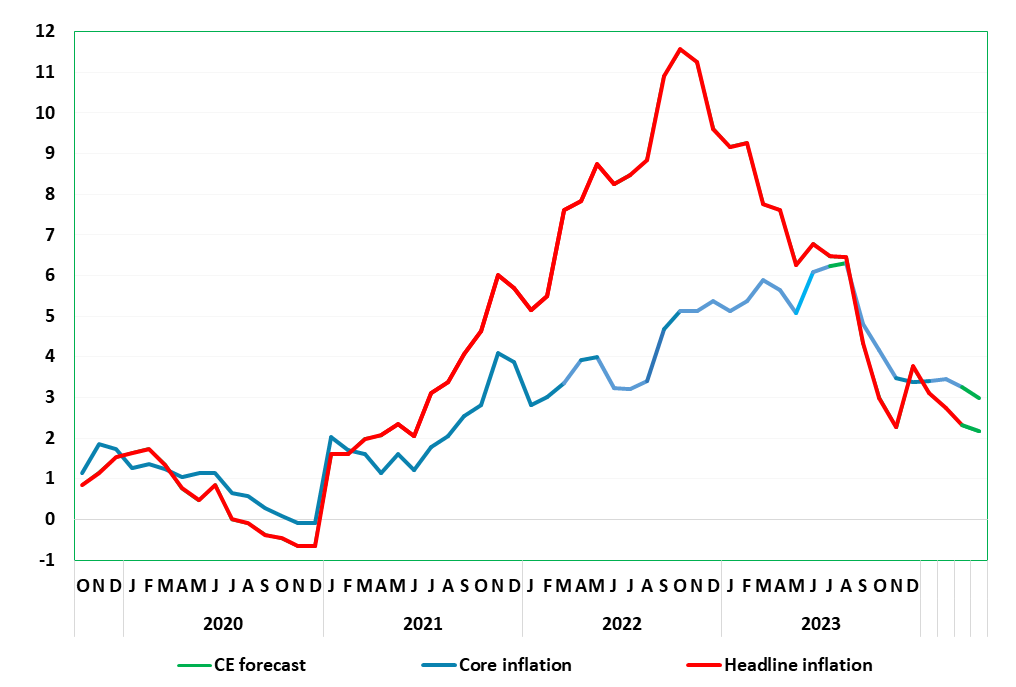

Very much having affected ECB thinking, there has been repeated positive EZ news in the form of falling EZ HICP inflation and somewhat broadly so. This continued in the March HICP numbers, with the 0.2 ppt drops in both headline and core being a notch more sizeable than most anticipated. Regardless,

April 22, 2024

German Data Preview (Apr 29): Inflation Drop to Continue Amid Less Resilient Services?

April 22, 2024 12:58 PM UTC

As we have repeatedly underlined, base effects continue to distort the German HICP/CPI readings, but the March data came in a notch below expectations for a third successive month. Indeed, it fell from 2.7% to a 33-month low of 2.3% in the March HICP data, dominated by a clear fall in food inflati

April 11, 2024

ECB Review: ECB Hums Easing Tune for June

April 11, 2024 1:58 PM UTC

Surprising hardly anyone, the ECB is preparing to cut official rates, after what are now five successive stable policy decisions. It explicitly suggested that it could be appropriate to reduce the current level of monetary policy restriction, a policy hint backed up by dropping its previous rhetoric

April 09, 2024

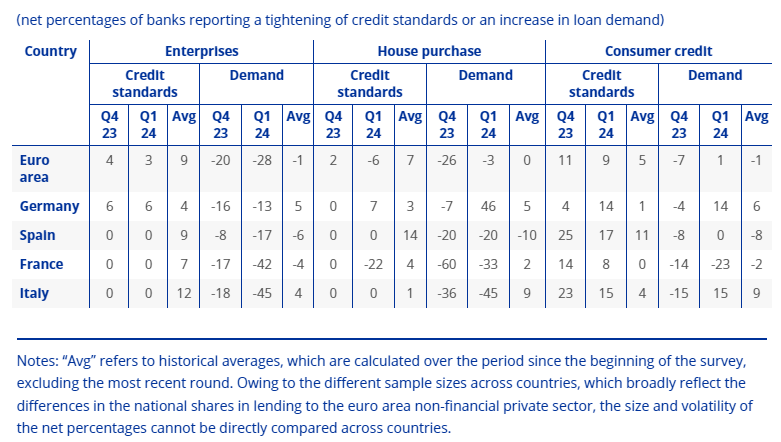

Eurozone Banks See Company Loan Demand Slump as ECB Unconventional Tightening Bites Further

April 9, 2024 9:22 AM UTC

While there may be few positive straws in the wind in the latest (April) 2024 bank lending survey (BLS), the ECB should fund the balance of results still troubling. Company credit demand slumped afresh amid rising interest rates and deferred capex plans. Admittedly, credit supply to firms tighte

April 04, 2024

ECB Preview (Apr 11): Still the Focus on Words Not Deeds – For Now!

April 4, 2024 12:22 PM UTC

As has been the case for several times now, the ECB meeting verdict due next Thursday (Apr 11) will be notable not for what the Council does but rather what is said just as at the March meeting whose minutes were released today. A fifth successive stable policy decision is very much expected, albe

April 03, 2024

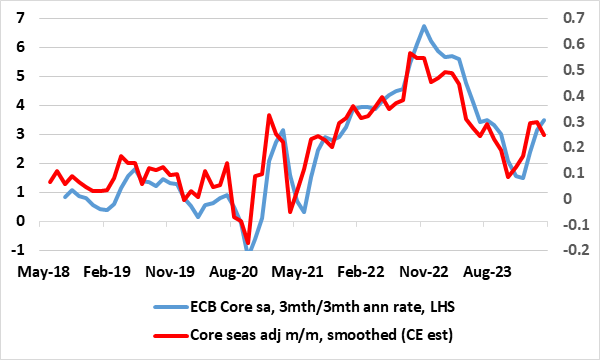

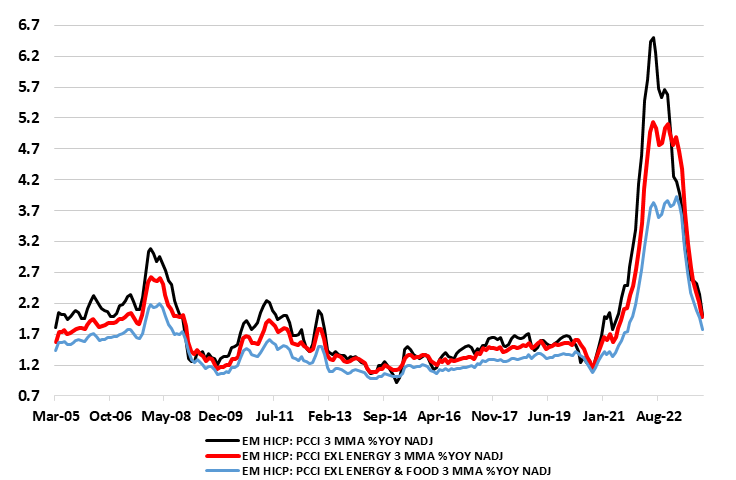

EZ HICP Review: Core Disinflation Flattening Out?

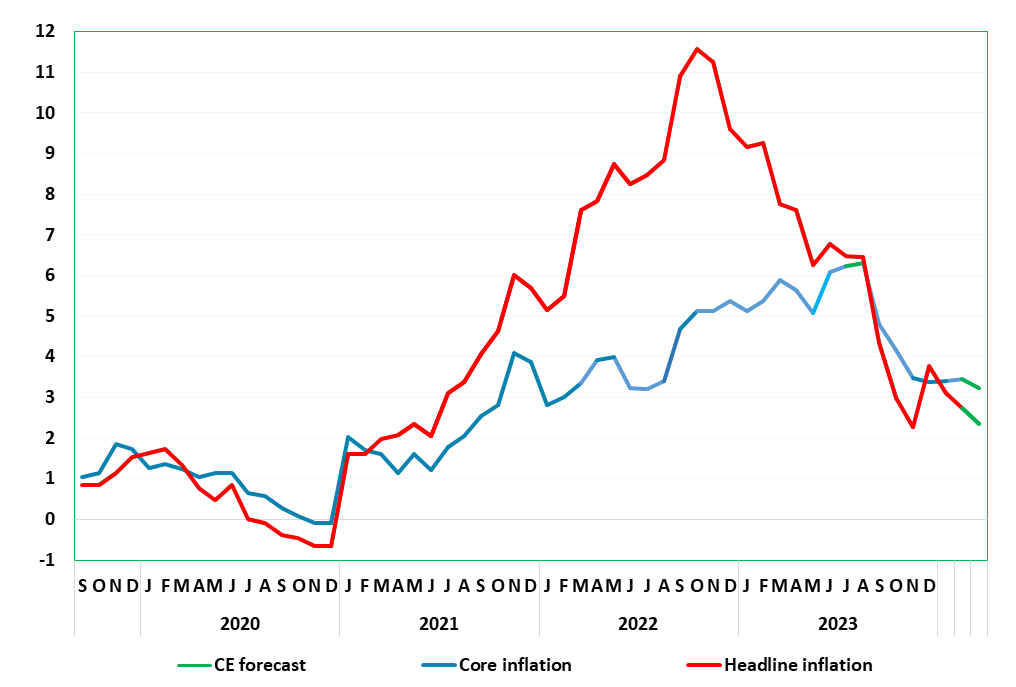

April 3, 2024 9:34 AM UTC

Very much having affected ECB thinking, there has been repeated positive EZ news in the form of falling inflation and somewhat broadly so. This continued in the March HICP numbers, with the 0.2 ppt drops in both headline and core being a notch more sizeable than most anticipated. Regardless, the hea

April 02, 2024

German Data Review: Inflation Drop Continues But Amid Still Resilient Services

April 2, 2024 12:19 PM UTC

As we have repeatedly underlined, base effects continue to distort the German HICP/CPI readings, but the March data came in a notch below expectations for a third successive month. Indeed, it fell from 2.7% to a 33-month low of 2.3% in the March HICP data, dominated by a clear fall in food inflati

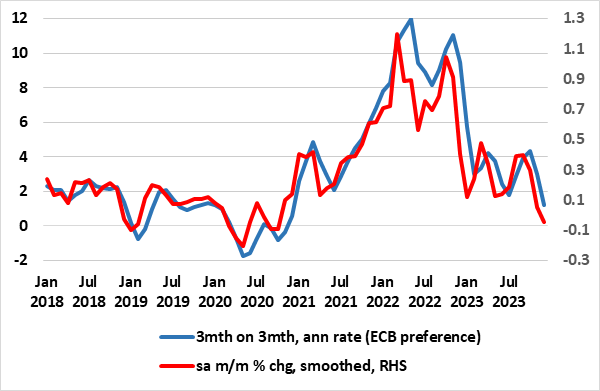

EZ: Labour Costs in Retreat Amid Hoarding and Workforce Jump

April 2, 2024 9:46 AM UTC

It is ever clearer how the labour market (and particularly labour costs) are the dominant theme for the ECB is assessing the policy backdrop and outlook. While HICP inflation continues to subside amid an economy backdrop which is flat at best, the labor market still looks apparently unmoved, with

March 27, 2024

EZ HICP Preview (Apr 3): Core Disinflation Signs Start to Flatten Out?

March 27, 2024 1:25 PM UTC

Enough to have affected ECB thinking, there has been repeated positive EZ news in the form of plunging inflation. This continued in the February numbers, albeit with the 0.2 ppt drops in both headline and core being less that most anticipated. Regardless, the headline, at 2.6%, continued its recent

March 26, 2024

German Data Preview (Apr 2): Inflation Drop to Continue Amid Less Resilient Services?

March 26, 2024 10:58 AM UTC

As we have repeatedly underlined, base effects continue to distort the German HICP/CPI readings, but the January data came in a notch below expectations, and reversed half of the surge in the y/y rate seen in December. And February data continued the downtrend, as the HICP rate fell from 3.1% to 2

March 25, 2024

March 22, 2024

Eurozone Outlook: ECB Finger on Easing Trigger?

March 22, 2024 10:42 AM UTC

· Our GDP outlook remains somewhat less below consensus and ECB thinking than envisaged three months ago, as other forecasters have reduced projections! Regardless, ECB policy has caused an increase in the cost of credit, alongside a fall in supply of credit. The result is that the ec

March 07, 2024

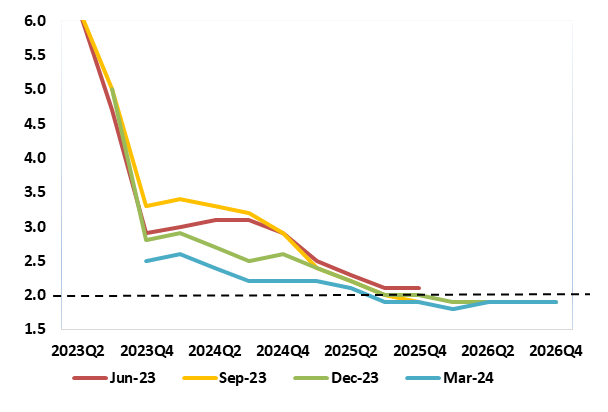

ECB Review: ECB Bowing to Markets?

March 7, 2024 3:36 PM UTC

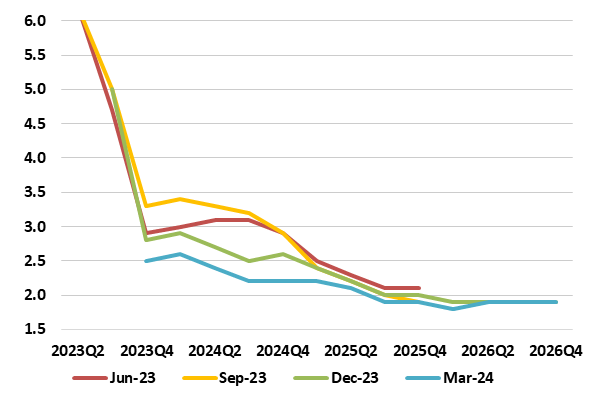

With the ECB staff updated forecasts pointing to headline inflation below target somewhat earlier, now in H2 2025 and then through 2026, and the core rate at target on the basis of market rate pricing of future official rates two years hence some 150 bp below current levels, this implies a tacit Cou

March 04, 2024

ECB Preview (Mar 7): Caution Still the Council Watchword

March 4, 2024 10:45 AM UTC

Once again the ECB meeting verdict due next Thursday (Mar 7) will be notable not for what the Council does (save for downward tweaks to its projections (Figure 1)) but rather what is said. A fourth successive stable policy decision is unambiguously expected. This will come alongside a reaffirmat

March 01, 2024

EZ HICP Review: Core Disinflation Signs Start to Flatten Out?

March 1, 2024 10:41 AM UTC

There has been repeated positive EZ news in the form of plunging inflation. This continued in the February numbers, albeit with the 0.2 ppt drops in both headline and core being less that most anticipated and with some hints that core disinflation may be marked. Regardless, the headline, at 2.6%, co

February 29, 2024

German Data Review: Inflation Drop Continues But Still Resilient Services?

February 29, 2024 1:13 PM UTC

Base effects continue to distort the German HICP/CPI readings, but the January data came in a notch below expectations, and reversed half of the surge in the y/y rate seen in December. And February data continued the downtrend, as the HICP rate fell from 3.1% to 2.7%, but with no further drop in t

February 28, 2024

Eurozone: Retailers’ Margins – the Profits of Gloom?

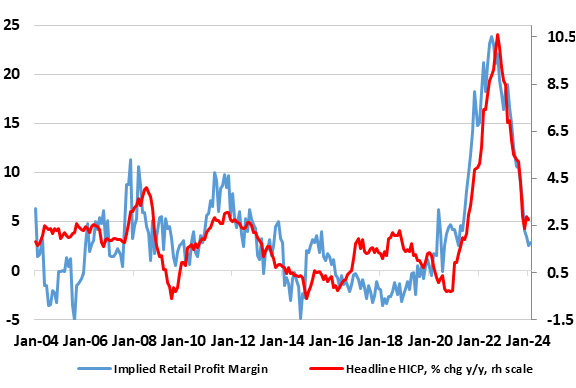

February 28, 2024 2:03 PM UTC

For all the ECB focus on the wage picture as the key factor shaping how HICP inflation may fare, the ECB has admitted to ‘significant uncertainty surrounding the link between wages and price-setting’. Productivity is one obvious other important consideration albeit probably the main alternative

February 27, 2024

Eurozone: Credit Weakness Deepens Afresh

February 27, 2024 10:47 AM UTC

The ECB faces an important few weeks, not least with the looming policy assessment and projection update due on Mar 7. Some downgrade to the real economy and inflation outlook (at least for the next 1-2 years) seems to be on the cards, albeit where the ECB hawks may regard the extent of any downwa

February 26, 2024

February 23, 2024

EZ HICP Preview (Mar 1): More Core Disinflation Signs As Services Inflation Slows?

February 23, 2024 9:50 AM UTC

There has been repeated positive EZ news in the form of plunging inflation. This continued in the January numbers, albeit with the 0.1 ppt drops in both headline and core being less that most anticipated. As a result, the headline, at 2.8%, resumed its recent decline having risen to 2.9% in December

February 22, 2024

ECB January Council Meeting Account Review: Clearer Need to Assess Market Rates Thinking

February 22, 2024 1:37 PM UTC

Unsurprisingly, the account of the January 24-25 ECB Council meeting was interesting is anticipating some downward revision to growth and inflation projections at the looming Mar 7 meeting. Moreover, it was noted that market rate thinking was in part an endogenous reaction and thus needed to be ca

February 21, 2024

German Data Preview (Feb 29): Inflation Drop Broadens Out to Services?

February 21, 2024 11:18 AM UTC

Base effects continue to distort the German HICP/CPI readings, but the January data came in a notch below expectations, and reversed half of the surge in the y/y rate seen in December. Indeed, the HICP rate fell 0.7 ppt to 3.1% and the CPI core down a notch to 3.1% as the headline CPI rate dropped

February 20, 2024

ECB – What is it Actually Targeting as it Assesses Price Persistence?

February 20, 2024 10:24 AM UTC

The ECB remit is targeting an inflation rate of 2% over the medium term. Implicit in this is that this is measured on a moving y/y basis. However, there is nothing sacrosanct in this as the ECB is starting to be more open about using shorter-term measures, albeit more as indicators of price mome

February 06, 2024

Eurozone: The Last Mile, Price Persistence and the Supplies Surprise

February 6, 2024 11:34 AM UTC

That the EZ economy is bordering on recession has obviously been a factor in the ever clearer and broad disinflation process seen of late. But we would argue (and many DM central banks would empathize) that it has been easing supply problems that has been the main factor. This better supply back

February 01, 2024

EZ HICP Review: More Core Disinflation Signs But Services Inflation More Stubborn?

February 1, 2024 10:26 AM UTC

There has been repeated positive EZ news in the form of plunging inflation. This continued in the January numbers, albeit with the 0.1 ppt drops in both headline and core being less that most anticipated. As a result, the headline, at 2.8%, resumed its recent decline having risen to 2.9% in December

January 31, 2024

German Data Review: Inflation Drop Resumes

January 31, 2024 1:28 PM UTC

Base effects continue to distort the German HICP/CPI readings, but the January data came in a notch below expectations, and reversed half of the surge in the y/y rate seen in December. Indeed, the HICP rate fell 0.7 ppt to 3.1% and the CPI core down a notch to 3.1% as the headline CPI rate dropped

January 30, 2024

Eurozone GDP Review: GDP – Divergent Weakness?

January 30, 2024 10:27 AM UTC

According to official national accounts data, the EZ economy has avoided recession, at least formally albeit against a backdrop of marked, if not increasing national divergence. Overall the flat q/q EZ GDP 4 reading was a notch below ECB thinking but a notch above consensus but this reflected mark

January 29, 2024

ECB Doves Coo Louder?

January 29, 2024 11:16 AM UTC

That high-profile ECB Council members are now talking both more clearly and openly about possible near-term rate cuts is of little surprise. It does fit in with both what was said and that was not said after last week’s Council press conference. Not least are week-end comments made by BoF Gove

January 25, 2024

ECB Review: Half Hearted Defence of Policy?

January 25, 2024 3:21 PM UTC

Unsurprisingly this latest ECB meeting was not notable for what the Council did but rather what is said. This third successive stable policy decision was unambiguously expected as was the more formal attempt to redirect market thinking that still prices 50 bp rate cutting by mid-year. Thus, it s

January 24, 2024

EZ HICP Preview (Feb 1): More Core Disinflation Signs As Headline HICP Fall Resumes?

January 24, 2024 3:24 PM UTC

There has been repeated positive EZ news in the form of plunging inflation. After coming in lower than envisaged for the third successive month, the December HICP inflation instead were in line with consensus thinking. Having dropped 0.5 ppt to a 28-month low of 2.4% in November, this was exactly

January 23, 2024

German Data Preview (Jan 31): More of Them Pesky Base Effects?

January 23, 2024 4:11 PM UTC

More base effects will distort the upcoming January HICP/CPI readings, pulling the headline back down, but the core rate higher, all adding to recent volatility. Indeed, the headline HICP in November eased 0.7 ppt to 2.3%, a 29-month low, with the core dropping by 0.7 ppt to 3.5%. However, last

January 18, 2024

ECB Minutes; Rate Cuts Seen But Not Heard?

January 18, 2024 2:22 PM UTC

In the press conference following the Dec 14 ECB Council meeting, President Lagarde was adamant that ‘we did not discuss rate cuts at all. No discussion, no debate on this issue’. But the just-released account of the meeting suggest that rate cuts may not have been formally spoken about, but t

January 17, 2024

ECB Meeting Preview: Summertime and the Living is Easing

January 17, 2024 12:22 PM UTC

Once again the looming ECB meeting (January 25) is one where markets are not preoccupied with what the Council will do but rather what is said. Stable policy is just about nailed on, but the question is whether there will be any more formal attempt to redirect market thinking that still prices in

January 16, 2024

EZ: Misleading Signals in Record Low Jobless Rates

January 16, 2024 2:16 PM UTC

While HICP inflation continues to subside amid an economy backdrop which is flat at best, and shrinking on a domestic basis, the labor market still looks apparently unmoved. Indeed, the EZ jobless rate has just returned to a record-low of 6.4%, hinting at labor market tightness that will perturb ECB

January 12, 2024

Eurozone Outlook: A Different Inflation Story?

January 12, 2024 11:13 AM UTC

Our Forecasts

Risks to Our Views

Eurozone: Price Pressures Receding Clearly

That the EZ economy is probably in recession, albeit a modest one, misses the point as the zero growth of the last year would have been some two ppt weaker were it not for the slump in imports. This is important as it not onl